The chart below tracks the unfunded liabilities of DeKalb’s Illinois Municipal Retirement Fund (IMRF), police (PD), and fire (FD) pensions.

We expect total pension liabilities will go up with raises, cost of living adjustments, etc. However, the unfunded portions of the liabilities should not. Actuarially determined annual pension contributions are supposed to ensure they don’t rise. Yet you can see by the chart that unfunded liabilities for police and fire climbed steadily for a generation. We’ve now accumulated some $126 million in liability debt. One of the consequences is this year’s contribution total of $9.7 million, which will gobble more than a quarter of the city’s operating budget.

However, the chart also indicates that someone began applying the brakes in 2018. It’s important to explain this so we can support policies that continue the trend to reduce unfunded liabilities.

Factors

Let’s start by busting a myth. People believe the reason we are so far behind on pensions is because the city did not make the required contributions. For most years I looked at, that is untrue. The problem is the amounts required were insufficient.

How did that happen? There are a lot of considerations in determining annual contributions. For example, there are assumptions based on compensation, numbers of retirements, and member mortality. If the unfunded liability of a pension rises in a given year, it means one or more of the assumptions in calculating the contribution was faulty. When faults happen year after year, it’s called a “structural flaw.”

I’ve gathered from years of pension discussions of DeKalb’s city council and its finance advisory committee (FAC) that the mortality tables the city was using required correcting because retirees don’t die as early as they used to. Another important issue is investment returns. Police and fire pensions used an 8% assumption for return on investment for at least 8 years; but two recessions hitting in the first decade of this century, along with statutory requirements for conservative investments in these funds, made that target virtually impossible to hit.

While the city has little control over IMRF assumptions, all it takes is a council vote to change the investment return assumption for police and fire. The rate was changed to 7.5% in 2012 and to 7.0% in 2017, and along with a couple of recent, decent investment years, we suddenly are seeing small reversals in the unfunded liabilities.

Drawing again from public budget discussions, I would credit the FAC for helping effect the assumption changes. I’m not sure they would have occurred otherwise, because it would have required management and council to act strategically on their own, and historically they’re not good at that. FAC provides political cover as well as good advice (and btw this is another reason it’s a shame FAC is not currently occupied at more than budget rubberstamping).

A Model for the Future

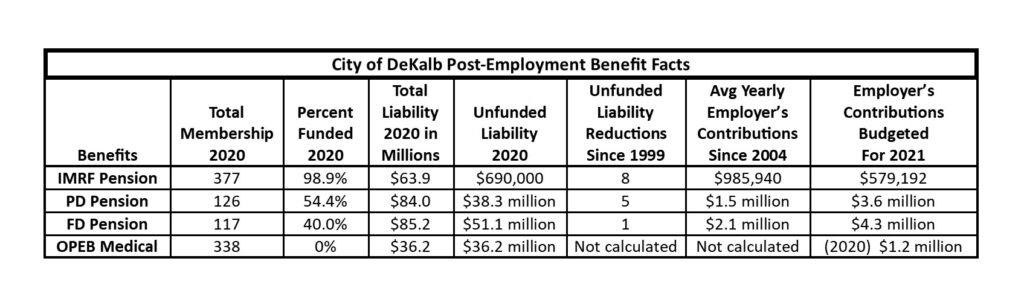

Meanwhile, the IMRF investment returns assumption was at or near 7.5% until 2018, when it was shifted to 7.25%. IMRF performance has consistently exceeded the others’ and the latest adjustment has landed it within striking distance of eliminating unfunded liability. Making comparisons using the table below, you can get an idea of the difference that paying down the liability debt can bring to the annual contribution.

It’s appropriate to include Other Post Employment Benefits (OPEB) because this medical benefits program for retirees also has issues with an escalating unfunded liability and we tend to forget it exists. We will revisit OPEB at some point.

For now, though, let’s keep in mind that the investment rate of return assumption for the police and fire pensions appears to be key in taming unfunded liabilities. It follows we should resist raising the rate assumption in this market and with the current investment mixes, and insist the city act more nimbly when the assumptions aren’t closing the gap.

Sources: comprehensive annual financial reports and annual budgets.